Bureaucratic bookkeeping may inadvertently grind Virginia solar development to a halt. The State government is assessing this issue, and we understand the state will issue a decision in due course. The following is the second of three installments highlighting SolUnesco’s research on the Virginia Composite Index and its impact on solar electric generation. To download our complete findings, click here

HOW IS SOLAR TAXED?

Covered in Part One of this series, the Composite Index (CI) may ignore the solar tax exemption when determining a county’s ability to earn tax revenue. Ignoring the tax exemption likely results in a Net Revenue loss. Due to solar generation’s non-polluting attributes, the state provides tax exemptions consistent with other pollution control equipment.

The following provides the relevant pieces of legislation regarding tax treatment for solar generating facilities:

- VA Code § 58.1-2600

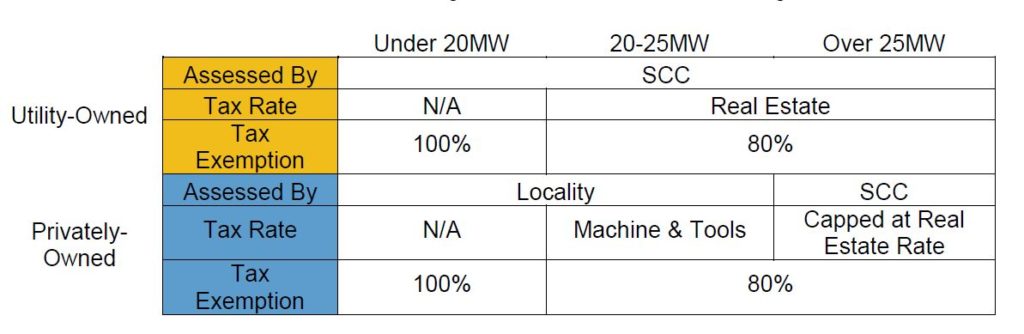

- Anyone who owns an electric generation facility over 25MW is an “Electric Supplier”

- The property of Electric Suppliers is assessed by the SCC.

- VA Code § 58.1-2606

- All property owned by Public Service Corporations (utilities) is taxed at the real estate rate.

- The tax on generating equipment owned by Electric Suppliers is capped at the real estate tax rate.

- VA Code § 58.1-3660

- Solar is considered Certified Pollution Control Equipment

- Solar under 20MWac is 100% tax-exempt

- Solar over 20MWac is 80% tax-exempt if it is put in service after January 1, 2017

The combination of these sections of the Virginia code results in the following tax matrix for utility-scale solar:

Hence, the Virginia code results in the following outcomes and uncertainty for solar generating facilities greater than 25 MWs:

- Inclusion in the CI as Public Service Corporation property,

- 80% tax exemption as pollution control equipment, and

- Uncertainty whether the CI will value the full value or the taxable value

A conclusion to this series is to follow in the coming week.

Leave A Comment